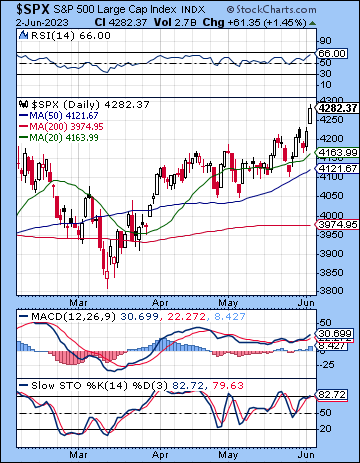

(4 June 2023) Stocks pushed higher last week following the debt ceiling deal and Friday’s strong NFP jobs report. The S&P 500 gained almost 2% on the week to 4282 while the Nasdaq-100 finished at 14,546. This bullish outcome was quite unexpected as I thought we might have seen deeper midweek selling around the Mars-Saturn alignment. While Wednesday was lower after Tuesday’s lackluster close, buyers stepped in once again on Thursday and took the indexes higher which coincided with the bullish late week Venus-Neptune alignment.

(4 June 2023) Stocks pushed higher last week following the debt ceiling deal and Friday’s strong NFP jobs report. The S&P 500 gained almost 2% on the week to 4282 while the Nasdaq-100 finished at 14,546. This bullish outcome was quite unexpected as I thought we might have seen deeper midweek selling around the Mars-Saturn alignment. While Wednesday was lower after Tuesday’s lackluster close, buyers stepped in once again on Thursday and took the indexes higher which coincided with the bullish late week Venus-Neptune alignment.

While the resolution of the debt ceiling negotiations has removed a major source of uncertainty, there remain some stubborn questions for markets to consider. For example, now that the US Treasury can legally borrow more money, how will the bond market absorb the fresh issuance of debt without upsetting the bullish flow of liquidity? With over $100 Billion in new Treasuries up for auction this week, markets will be monitoring bond yields more closely than ever as increased bond supply usually translates into higher yields and hence less liquidity for stocks. As capital markets buy up more bonds, there will be less money left for equities, of course, which could weaken the current enthusiasm for stocks. And with the Fed reducing its balance sheet by another $50 Billion last week, the effects of quantitative tightening may have yet to run its course. Yields climbed on Friday after the strong jobs report hinted at further Fed rate increases, even if the odds for a hike at the June 14 FOMC meeting remained fairly muted at 28%. The divergence from the Fed and the market expectations hasn’t changed much in recent weeks, although more Fed members are now embracing the idea of skipping a hike, rather than initiating a conclusive pause in the tightening cycle. Nonetheless, if inflation stays sticky for the June 13 CPI report, there is some risk for unpleasant hawkish surprises from the Fed.

The planetary outlook is uncertain. I must admit I am a puzzled by the absence of any meaningful pullback in the blue chip indexes so far. While we did get some of the anticipated weakness in May in the broader indexes such as the NYSE Composite, the Russell 2000 and the Equal Weighted S&P 500, the SPX and the Nasdaq have continued to power higher. The progressed cycles are looking mixed for early June and do not present strong evidence for an imminent correction…

Click here to subscribe and read the rest of this week’s newsletter